Impact from COVID-19 in Latin America: widespread shock but with different recoveries

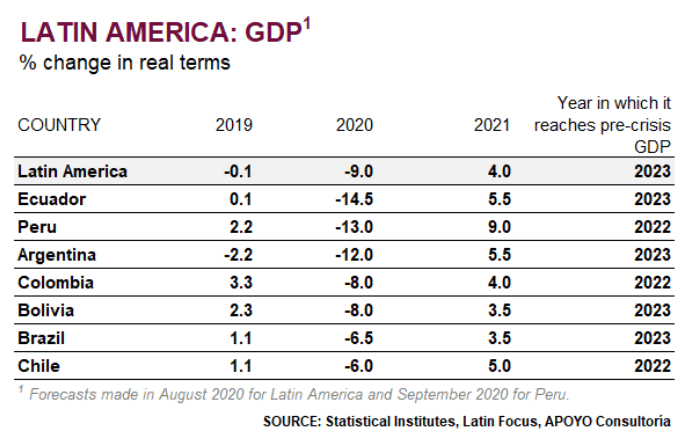

Latin America has been one of the regions most affected by the spread of COVID-19, both in terms of health and economy. To date, five of the ten countries with the highest number of deaths per million people are Latin American. Furthermore, the GDP of the region will contract close to 9% this year, almost twice as much as the average decline expected on a global level (5%).

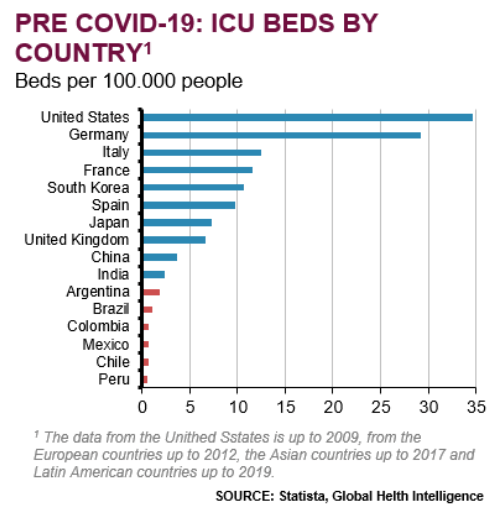

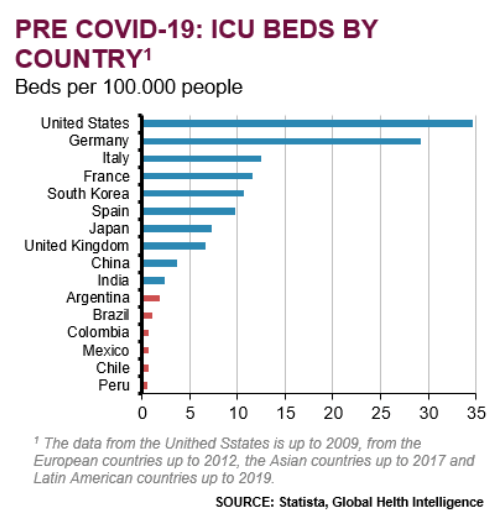

Structural weaknesses, such as deficiencies in the health care systems and high levels of informality and overcrowding are the reasons behind the severity of the crisis in the region. Before the emergency, the capacity of the health care systems to treat seriously ill patients was very limited (see graphic below). Additionally, high levels of informality and overcrowding in the region made the COVID-19 prevention protocols less effective.

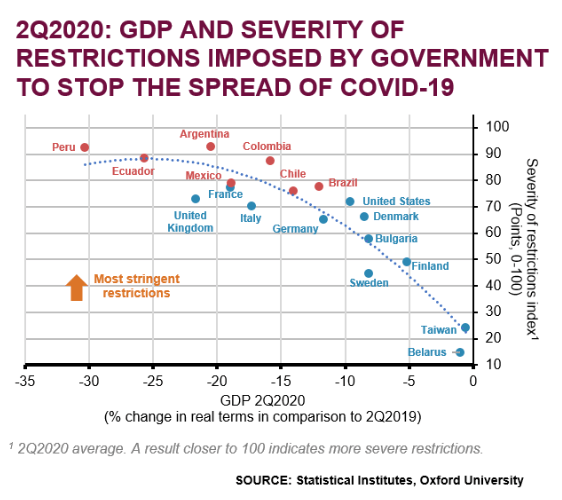

In the face of the high level of vulnerability in terms of health, Latin American governments implemented more drastic and longer quarantines than the rest of the world. As a consequence, the gridlock of economic activity was more widespread and caused a big fall in income, both for households and businesses.

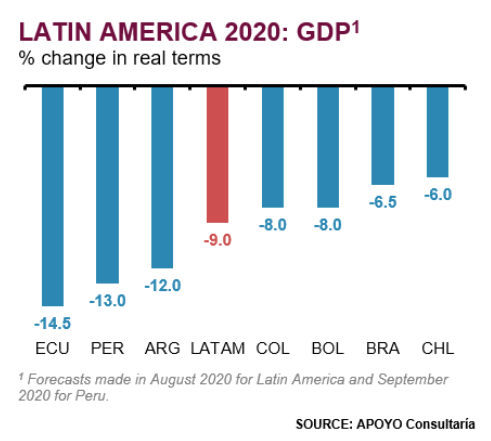

Thus, even though many countries in the region will experience a strong economic recession this year, the contraction will be more severe in Peru, Ecuador and Argentina. Firstly, the economic contraction has been stronger in these countries due to the severity of their containment measures: only essential activities were permitted, such as financial services, and the sale and production of food and medicine. Moreover, the reactivation of the economy was slower here, seeing as longer quarantines were implemented (nation-wide and for over 80 days). Secondly, for the remainder of the year, the capacity of reactivating the economy by higher public spending is limited. In the case of Argentina and Ecuador, this is due to restricted access to external financing and limited room for expansive economic policy. Whereas, in Peru, despite possessing the fiscal resources, low levels of execution and delays in the implementation of measures will limit the impact of the public stimulus.

Starting next year, three factors will determine the different rate of economic recovery for the countries of the region: 1) the control of the virus, 2) the space for expansive economic policy, and 3) the political environment. Firstly, the capacity of the governments to contain the expansion of the virus will be key to avoid new measure of restriction of movement which would slow down economic recovery. In recent weeks, deaths caused by COVID-19 in countries like Peru, Colombia and Chile have started to decrease. In contrast, in Argentina and Brazil, the number of deaths continues to show an upward trend.

Secondly, in Argentina, Ecuador and Bolivia, the public sector will have little room to implement expansive economic policy to boost aggregate demand. Even though the fiscal balance sheets in all of the countries of the region will deteriorate, in the aforementioned public debt will reach a level which will hinder the access to financing. To make matters worse, these countries don’t have room to apply expansive monetary policy, either. In contrast, Chile and Peru will have less of an urgent need to withdraw their economic stimuli, since they have more space in their fiscal sphere and monetary policy.

Thirdly, the political front could be a significant limitation to the economic recovery of countries like Peru, Argentina, Bolivia, Ecuador and Brazil, due to the difficulties in reaching basic consensuses as well as the uncertainty, which would affect private investment. Furthermore, given the context of strong social unrest and the political crisis, there’s a risk a government with populist tendencies is elected in Bolivia (where the general election should be taking place in October 2020), Peru, Chile and Ecuador (where the general election is taking place in 2021) which could propose policies affecting several economic sectors.

In summary, the countries that are likely to take longer to reach their pre-crisis GDP are Argentina, Ecuador and Bolivia.

Due to this context, the challenges that the new administrations in the region will have to face are going to be enormous, since social unrest will increase in an environment of reduced fiscal space to attend to citizens’ demands. The crisis caused by COVID-19 is going to increase poverty and inequality across the region, after several years of registering improvements. This will lead to citizens demanding better public services and better social protection. To attend to this, in a context of less fiscal space, it will be key to achieve a minimum of political agreements to implement effective and sustainable measures.

OUR PERSPECTIVE

Peru's economic growth was dynamic in Q1 2025, although international environment risks have intensified.

The economy maintained a solid growth pace in Q1 2025, around 3.8%, slightly above expectations. Primary sectors, such as agro-exports and fishing, continued to rebound, although they were still affected by weather conditions in Q1 2024.

Political pressure on the government intensifies with the censure of Santivañez and new episodes of protest.

This month, the political agenda has once again focused on citizen insecurity. The death of a singer from a well-known musical group, allegedly at the hands of extortionists, sparked renewed criticism of the Minister of the Interior, who was censured by Congress, which in turn triggered new protests.

Resumption of Congressional Functions: Oversight, Electoral Reforms, and Key Projects on the Short-Term Agenda

Despite growing criticism, President Dina Boluarte remains reluctant to remove him from office, as Santivañez plays a key role in her efforts to obstruct investigations against her and her inner circle, including her brother Nicanor Boluarte.